An introduction to the U.S. healthcare system as "harder than rocket science" because it's a massively expensive and underperforming system plagued by "consolidated fragmentation." Despite enormous spending, outcomes lag behind other developed nations. The core issue is that the major players—insurers, hospitals, and providers—have grown into powerful, competing silos. This creates a gridlock that stifles innovation and prevents them from working together effectively to improve patient health, as each entity focuses on its own financial advantage.

VBC Series··11 MIN READ·Last updated 2026.04.20

My grandfather, an engineer on NASA's Apollo missions, often joked that rocket science was simple: you just point the rocket in the right direction and light it. The real challenge was all the engineering and teamwork required to make that simple act possible. American healthcare presents a similar paradox.

The goal of navigating a patient through the right treatment should be straightforward. We have access to the best medical science in the world. But, we’ve made the launchpad into a toll road. Medical data is siloed in proprietary data systems, insurers not doctors decide what treatment a patient is ‘eligible’ to receive, specialist care is fragmented requiring hours on the phone…and patients sign the same consent form 120 billion times.

My aim with these posts is to untangle that web - why does it exist? What have I done to try to fix it and why didn’t it work? This is the story of what makes American healthcare feel harder than rocket science.

As a technology leader at forward thinking healthcare companies like Cityblock Health and Firsthand, I built platforms that delivered preventative care to tens of thousands of our system's most underserved individuals. We proved that new models could simultaneously improve outcomes and reduce costs. But, the landscape continues to change. The strategies that powered those successes are no longer sufficient in an era defined by AI, Medicaid eligibility changes and the market dominance of a few healthcare giants. I believe we need to take a new approach to healthcare data, business contracts, and health organizations.

Let's get started: Where are we now?

This first part gives an overview of the business of US healthcare in 2025. You can likely skip it if you already work in the industry.

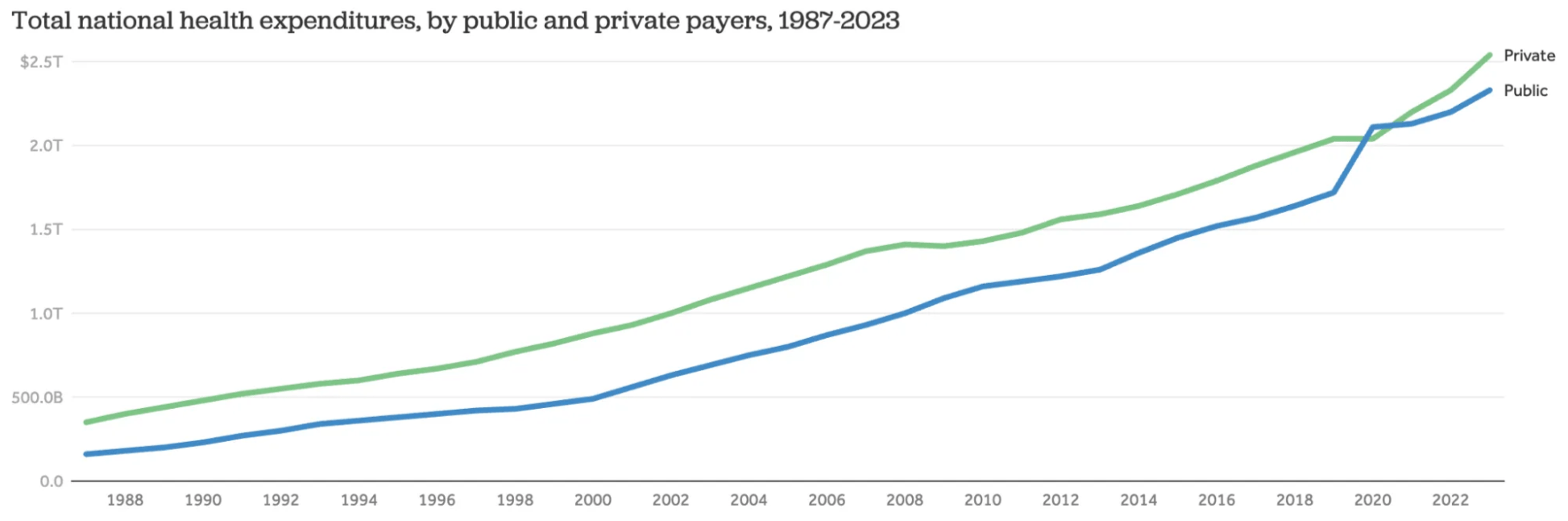

Healthcare is a massive industry and the largest employer in the United States, with over 22 million workers. It makes up 17.7% of the nation's total economic output (GDP) and is expected to reach 20% by 2032.

The growth in healthcare costs has far outpaced other industries. From 1996 to 2024, health insurance premiums increased by 339%, while average wages grew by only 126% (KFF Employer Health Benefits Survey). During that time, over half of the average employee's pay increase was absorbed by health insurance costs. As a result, the take-home pay for many Americans has not changed much in 30 years, despite major gains in productivity from new technology.

This huge and uneven growth in healthcare costs is one of the reasons most Americans feel so frustrated.

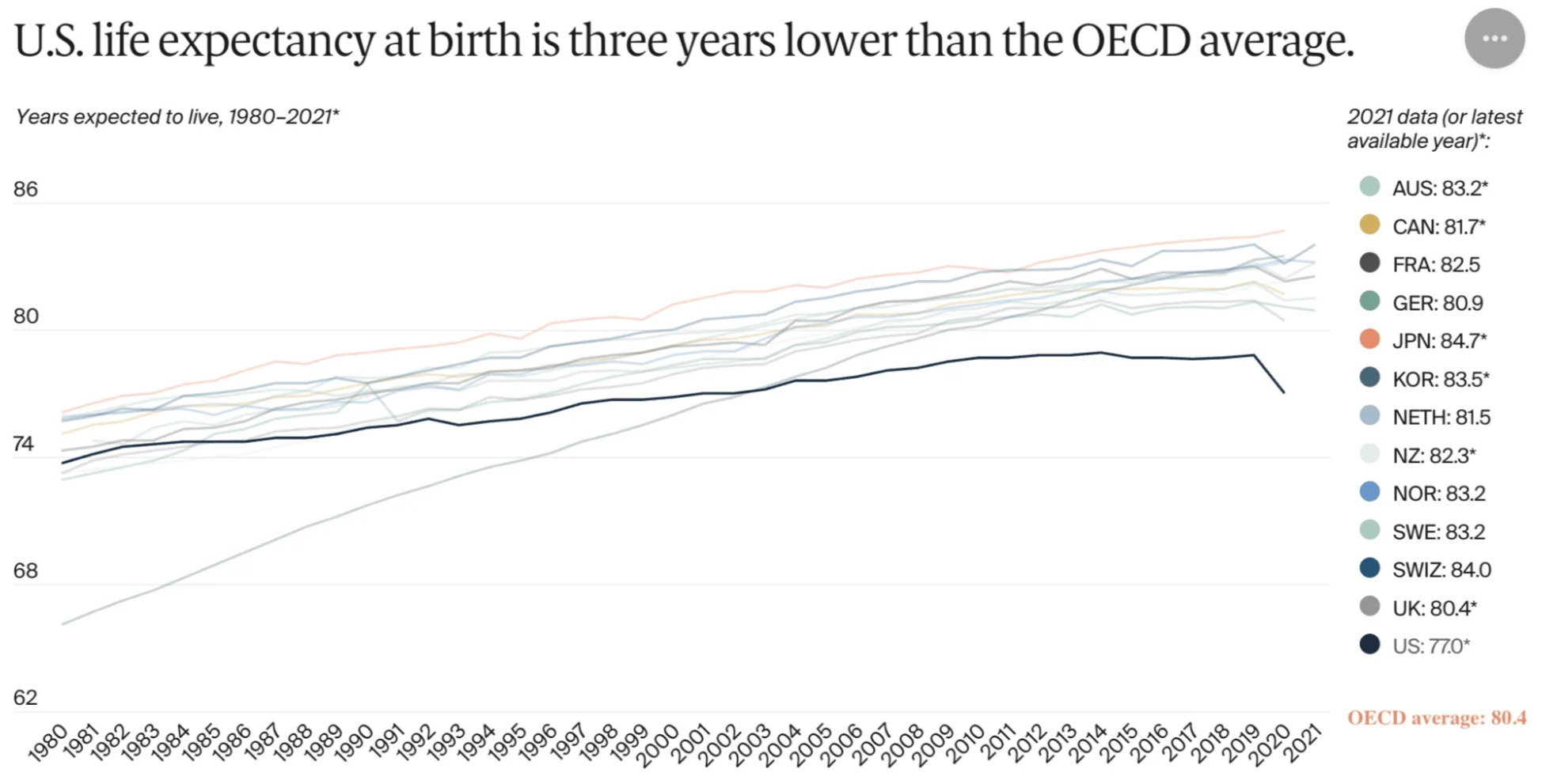

You'd hope that all that money spent would mean the U.S. has the best healthcare in the world. Well, that's not true for everyone.

A good way to see this is by looking at maternal mortality, which is how many women die during or after childbirth. It's often seen as a good way to tell how healthy a society is overall. Let's compare the U.S. rates with the UK. I'm not saying the UK system is perfect, just that it's a similar country to the U.S. and is more different than Canada.

In 2022, the US had 22 maternal deaths for every 100,000 live births. The UK had only 5.5. The UK achieves this while spending 10% of its GDP on healthcare, compared to the 17.7% spent in the US.

However, It is misleading to talk about a single "US healthcare system." A person's health is best predicted by the the zip code you were born. There are vast differences between states. For example, California's maternal death rate is half the national average at 10.5. Louisiana's rate is 37.3, which is similar to that of developing nations like Cuba or Mongolia. These wide gaps in health outcomes make it difficult to agree on national policies.

The big players

The basics

In short there are 5 may groups at play in American healthcare:

Patients/Consumers: The people who need healthcare.

Providers (Doctors, Hospitals, Clinics): Deliver the actual care.

Payers (Insurance Companies, Government Programs like Medicare/Medicaid): Pay for the care.

Pharmaceutical Companies/Medical Device Manufacturers: Develop and sell drugs and equipment.

Employers: Often facilitate insurance for employees and purchase healthcare products for them.

Before working in healthcare, I spent years managing engineering teams at startups like Artsy. One thing I learned is that structural problems often masquerade as people problems. We see this blame game happen all the time in healthcare ‘big pharma is evil!’, ‘UHC is evil’ etc. When a team is struggling, the instinct is to blame individuals, but the real issue is often structural. Everyone is acting rationally but they have different incentives and information. Healthcare's dysfunction follows the same pattern at a national scale. The players listed above are not incompetent. They are smart, well-funded organizations trapped in a structure where collaboration is expensive and not aligned with their quarterly earnings targets.

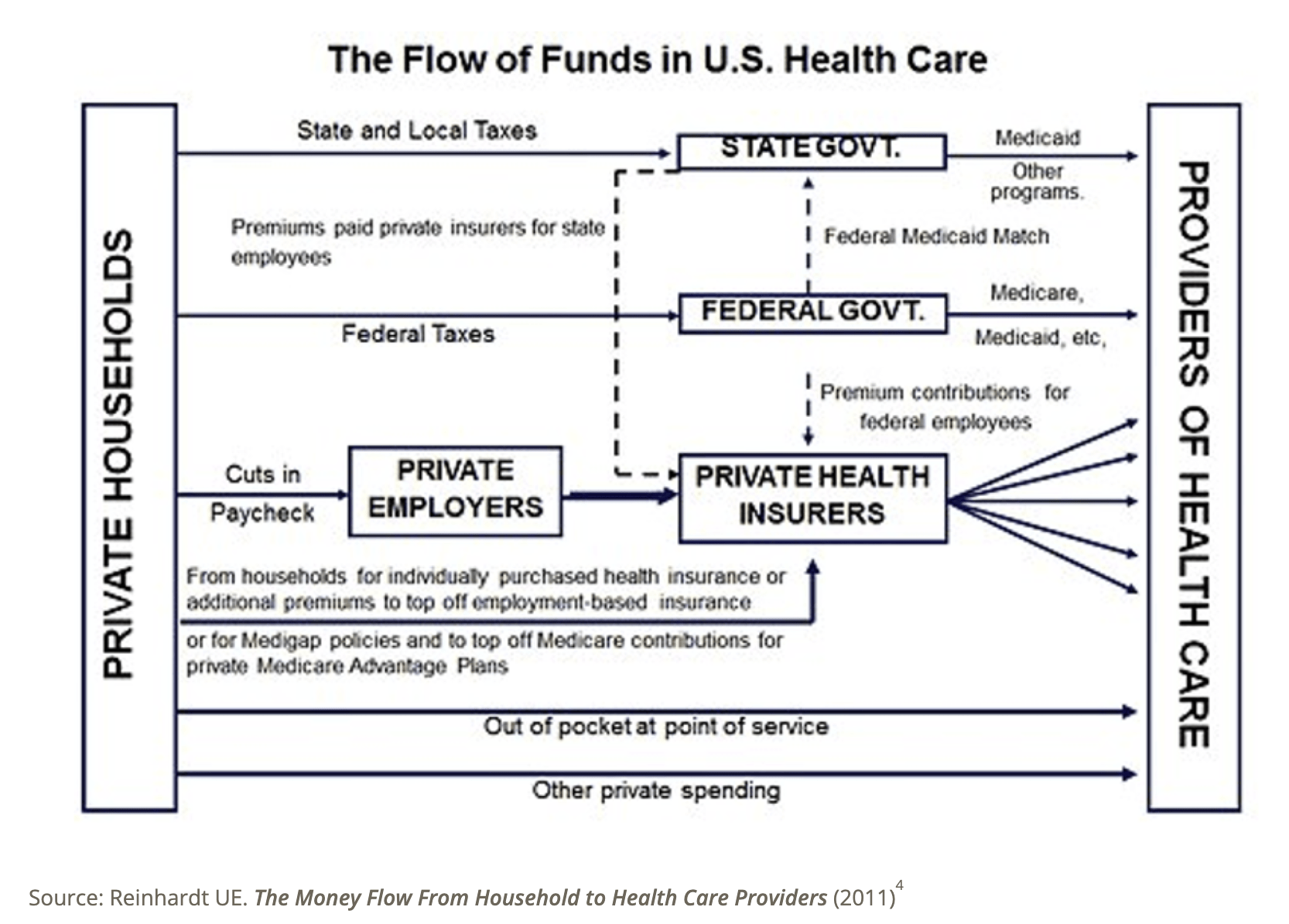

The big Players: Payers / Insurance companies

Payers, or insurance companies, are the most powerful group. All the money flows through them. Over the last 20 years, they have expanded from simply paying bills to actively managing care. They can deny treatments and reduce payments to providers they consider poor-performing.

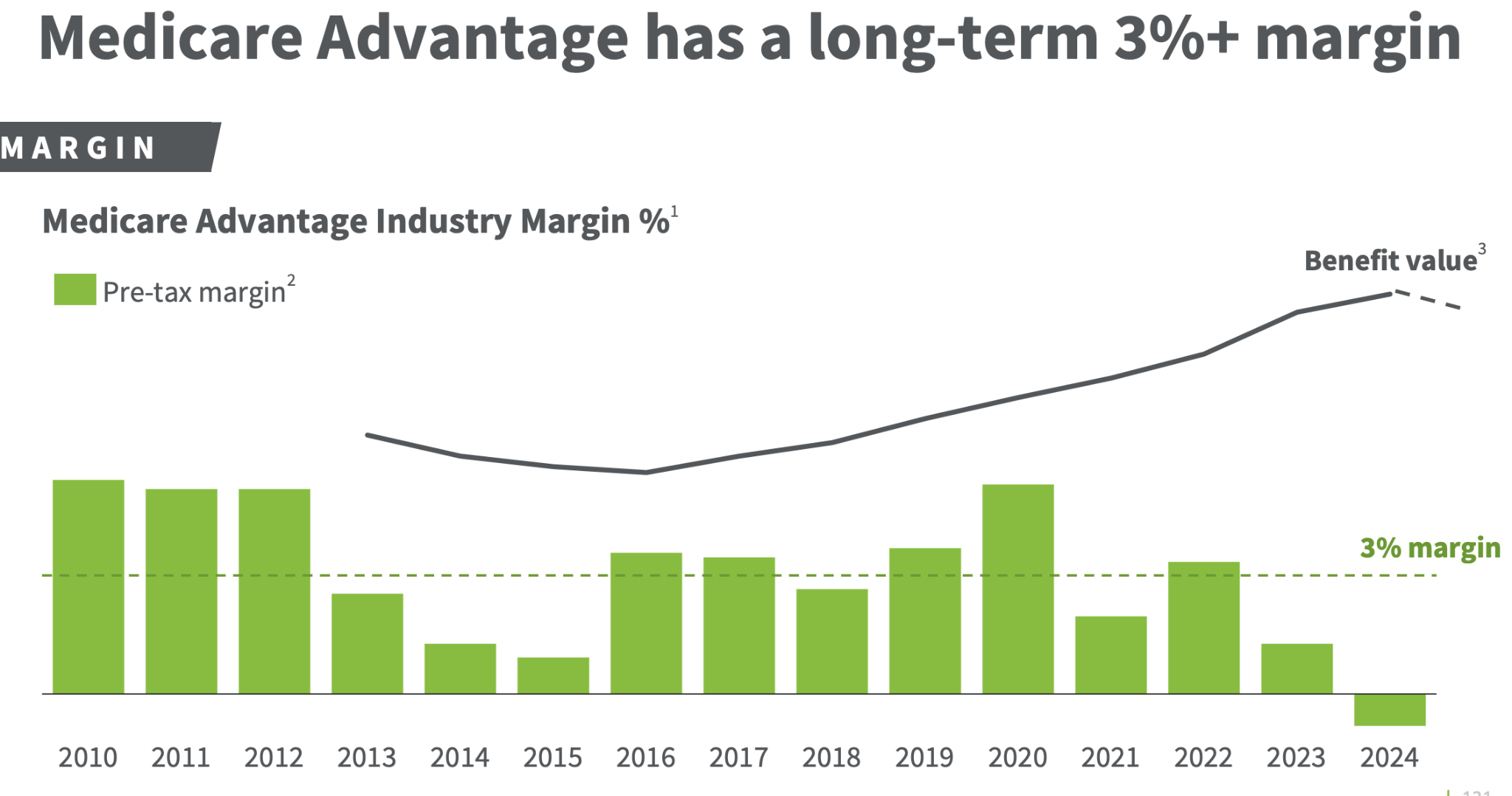

Insurance company revenues are staggering: UnitedHealth Group at $400 billion, CVS Health at $372 billion, and Cigna at $241 billion, and the list goes on. However, their profit margins (how much money they actually keep) are quite low and are similar to a restaurant, ranging from 1.5% to 3.8%. This is partly because they invest a lot in growth and research.

Growth has also come from Managed Medicaid and Medicare Advantage. These "managed" programs are where private insurance companies handle government-sponsored health benefits. This means that some of the $1.8 trillion spent on these government programs to flow through them. These programs connect patients with a network of doctors and hospitals, as an alternative to the traditional government system where every service is paid for separately. While these plans might reduce costs for people on these plans, they can also lead to higher costs for taxpayers, and it's not always clear if they actually save money in the long run.

The big players: Hospitals

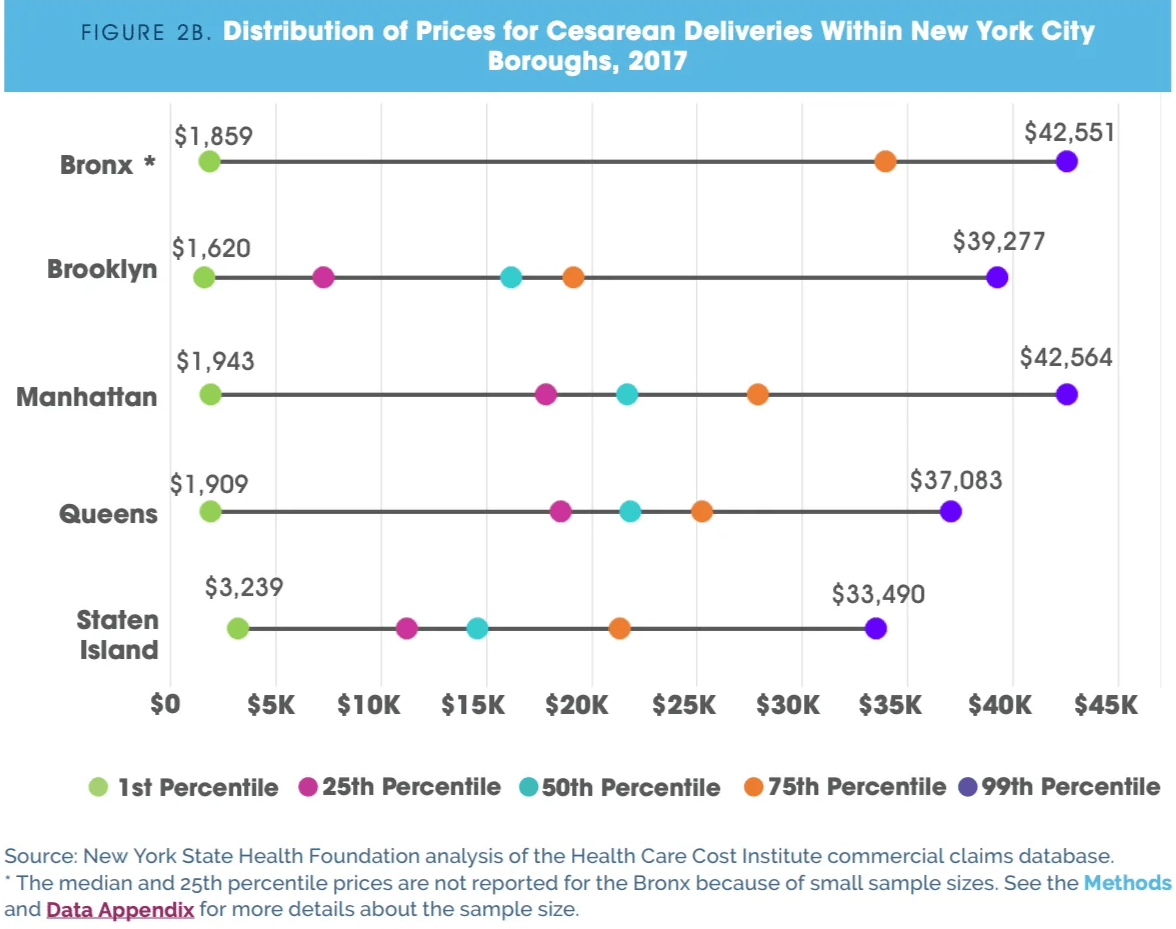

Hospitals have also grown into powerful economic engines through consolidation. For example, HCA Healthcare, the country's largest hospital system, had more revenue in 2023 than Netflix, Uber, and Starbucks combined. Key problems with hospitals are a lack of price transparency and a heavy focus on tasks related to billing. Patient information is often not shared between hospitals, doctors, and insurers, which makes coordinated care difficult.

Even though prices are now more transparent due to recent legislation, the costs vary wildly. For example in NYC, a C section at one hospital may cost you 20 times as much as at a different one down the street.

The big players: Providers

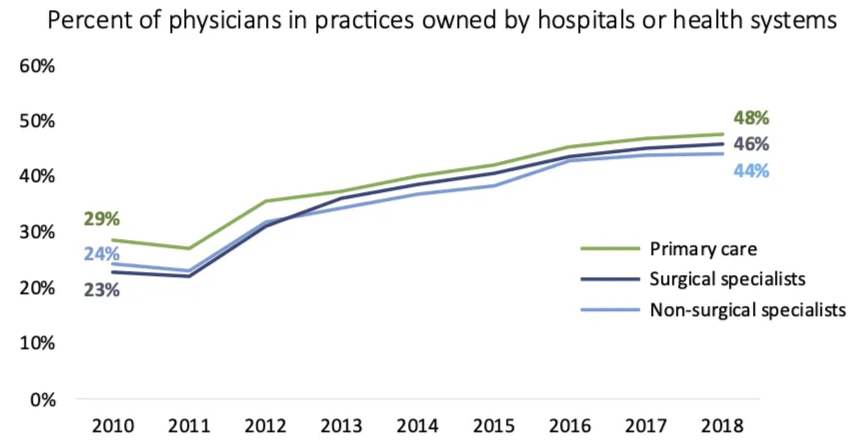

Providers like doctors have also seen major changes. Most physicians, around 75%, are now employed by hospitals or corporations, whereas 20 years ago they were almost all independent. Many have joined larger groups called Accountable Care Organizations (ACOs) to help coordinate care and meet performance goals. Practices now employ more support staff to handle the documentation required by electronic health records and complex payment models.

These larger groups help with better coordination of care among their doctors and can support each other in meeting "value-based care" goals, like Clinical Quality Measures. These measures look at things like how well doctors follow guidelines for preventive care (like vaccination rates or cancer screenings) and how well they manage long-term illnesses (like controlling blood pressure for patients with high blood pressure or A1c levels for diabetic patients).

The second big change for healthcare practices is the number and type of people who support each doctor. Currently, practices have about 4.79 support staff for every doctor. This ratio of support staff to doctors is a big topic and has changed quite a bit over the past 20-30 years. This is due to more documentation needed for electronic health records (EHRs), the need to report data to calculate all the performance measures mentioned above, and the shift toward doing more "care management," which is often called a Patient-Centered Medical Home (PCMH).

Today: Consolidated fragmentation

Over the last decade, every part of the healthcare system has consolidated. Insurers, hospitals, and provider groups have consolidated into a small number of powerful, separate entities.

I call this "consolidated fragmentation."

From their own fortresses, these groups argue over who pays when things go wrong, who gets rewarded when things go right, who controls patient data, and who pays for shared technology.

I've seen this gridlock play out in ways that are hard to explain to people outside of healthcare.

At a recent company, we helped people with severe mental health conditions. Our team and the insurance company agreed that long-acting injectable antipsychotics were the best treatment path for many of these patients. The medications are expensive, costing $5,000 or more per year, but they are a once a year treatment that is proven to reduce emergency room visits, hospitalizations, and overall medical cost.

Then policy changed. Medicaid eligibility rules shifted and patient churn increased. Insurance companies, facing the prospect that these patients might switch plans within months, lost interest in long-term health outcomes. They redirected us to get patients OFF of long-acting injectables and onto monthly generic pills costing $5 per month.

Here is the math the insurance company was doing: why invest $5,000 per year in a patient who might be on a different plan in six months? Let the next insurer (or the hospital) pay for their care.

Here is the math we were doing: these patients (often homeless, often in crisis — which is why they are on Medicaid!) are unlikely to reliably fill and take a daily generic medication. We know from experience that many will stop taking it. We know that when they do, they will end up in the emergency room. But by that time, they may no longer be on this insurance plan. They may no longer have Medicaid at all.

This is consolidated fragmentation. Every player is making a locally rational decision. The insurance company is managing its quarterly financials. The pharmacy benefit manager is optimizing drug spend. The provider (where I worked in this example) is following the direction of the entity that pays us. And the patient, who was finally stable, is caught in the middle of a system where no single entity is accountable for their long-term health.

This structure creates gridlock and consolidation of each entity (1-2 insurance companies per-state for example). While new technology like AI should make innovation easier, the most logical financial move for each group is to seek an advantage over the others. This comes at the expense of working together for patient health.

As a consumer, I want all these companies trying to innovate to find lowest cost and highest value ways to keep me as healthy as possible.

My grandfather used to say launching a rocket was easy - you just point the rocket up and light it. The hard part was getting thousands of engineers, contractors, and government agencies to coordinate to actually get the rocket to the launchpad. NASA solved this with one mission control, shared telemetry, and a deadline that the entire country could see.

Healthcare has no mission control. It has three fortresses — insurers, hospitals, and providers — each with their own telemetry, their own definition of success, and their own financial incentive to guard their walls. The patient is the rocket, and nobody agrees on where it should be pointed.

In the next post, we will look at why a more integrated approach called "value-based care" might be the solution and why, even with the right intentions, it is proving harder than the moon landing. Check it out here.

This post details the value-based care is a model that pays providers to keep patients healthy and contrasts it with the traditional fee-for-service system. I argue that while the goal is simple, implementing it is "harder than rocket science." Drawing from my experience, the post details the extreme difficulties involved, including navigating multi-year contract negotiations with insurers, building a massive and complex operational system before seeing a single patient, and the immense challenge of aligning internal teams who often have conflicting goals. I argue that this operational gridlock makes it nearly impossible to create a scalable, efficient, and truly patient-centered system.

Your official health record is a useless mess, fragmented across different doctors and insurers. I argue that advertisers at companies like Google and Amazon know more about your daily life and habits than your own physician. Because this foundational data is so broken, new healthcare models like value-based care are failing, and simply applying AI won't fix the problem until the data itself is fixed.

Value-based care contracts are challenging due to lengthy negotiations, strict and evolving security demands (especially post-Change Healthcare), and rigid terms that hinder innovation. These issues create financial strain for startups, making value-based care primarily accessible to large, established healthcare entities. In a world rapidly changing due to AI and at the policy level, we should set a target of contracts taking 1 month rather than 1 year. My recommendation is for contract standardization and data sharing processes that are either centralized or fully open-sourced.

If I could start over with everything eight years in value-based care taught me, what would I build? Two things: a standardized contract and data broker that turns year-long negotiations into month-long ones, and a universal patient data layer that follows the patient across insurance plans instead of resetting to zero every time they switch. Only once that foundation exists does AI become useful rather than dangerous. Healthcare's hardest problem was never the medicine — it's the coordination, the same problem the Apollo program had to solve first.

§·More Reading

More Essays

On engineering leadership, value-based care, and the craft of building.

Every AI agent wakes up with amnesia. This post details the Kelp codebase which runs two completely separate memory systems, one for the coding agent and one for the product. I argue that truely useful AI memory is a real subsystem with tiers, citations, expiry dates, and garbage collection. The hardest part isn’t recall; it’s knowing what to keep, what to supersede, and when to throw something out.

This post argues that building successful software for value-based care (VBC) requires a shift in mindset: create a Customer Relationship Management (CRM) tool, not just a better Electronic Health Record (EHR). VBC realigns healthcare incentives around long-term patient outcomes, succeeding through proactive, relationship-based care rather than transactional services. Technology's role is to support this relationship by helping care teams orchestrate interventions effectively. The most valuable tools are often simple and pragmatic, focusing on the unique, core needs of the care model and enabling proactive management of patient health.

Reflections on pausing the contextual recommendation tool, Kelp, concluding that its goal—getting people the right information at the right time—is nearly impossible for a third-party app to achieve. The core problem is technical: without deep, OS-level access to user data and behavioral signals, recommendations remain mediocre. True contextual help must be built into the operating system itself. The key business takeaway was the need to solve a highly specific, paying use case for a narrow audience before attempting a broad, cross-platform solution.

This reflection on leadership in a hyper-growth startup argues that self-management is the most crucial skill. Management in such a chaotic environment is inherently reactive and emotionally draining, not strategic and proactive. The key to effectiveness is to abandon "ruinous empathy"—the futile attempt to please everyone—and instead fiercely conserve personal energy for high-impact moments. This is achieved by accepting failure and tradeoffs as constant, communicating them transparently, and focusing on maximizing success in key areas rather than fighting every fire.